In 2023, real estate stocks experienced a rollercoaster journey, mirroring broader market fluctuations. The year began on a shaky note, with both commercial and residential sectors feeling the pinch of rising interest rates. However, this downward trend pivoted in the latter half of the year as real estate pricing and Real Estate Investment Trusts (REITs) witnessed a significant upsurge, sparking optimism for 2024.

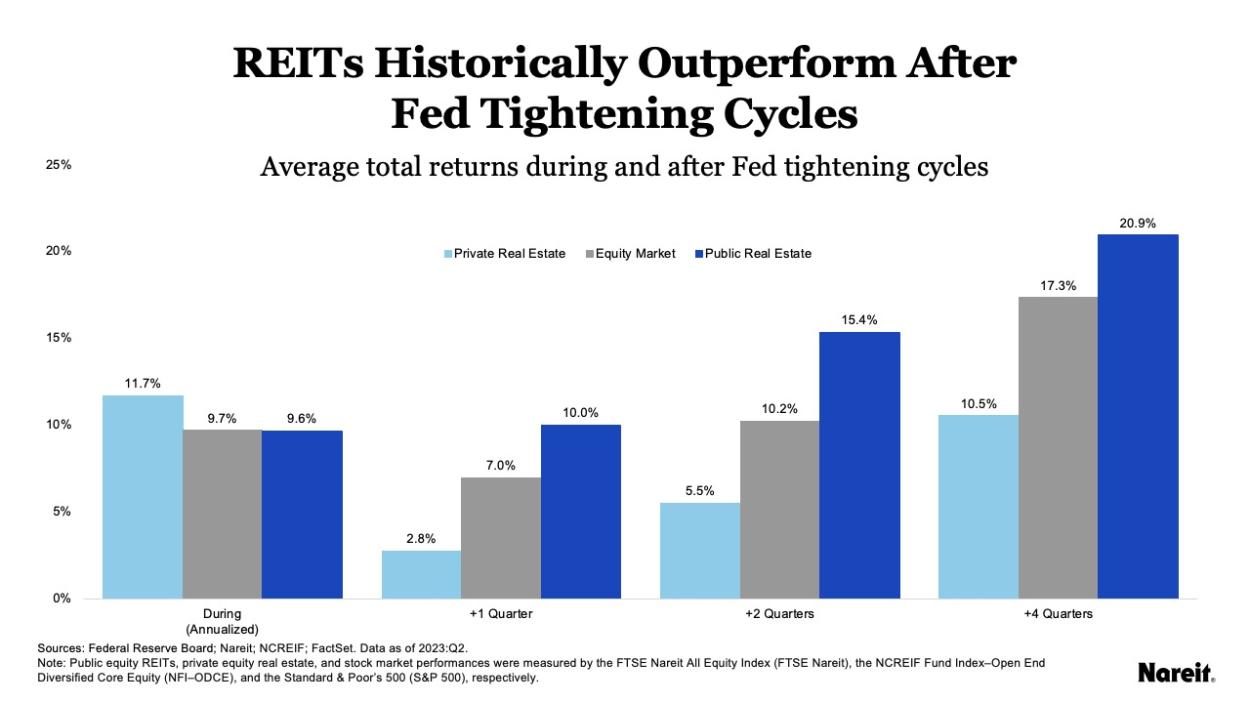

Historically, REITs have outperformed following Federal Reserve tightening cycles, averaging a 20.9% annual gain post-quantitative tightening. If the Federal Reserve halts rate hikes as rumored, real estate stocks and REITs are poised for potentially their best year in decades, offering a promising outlook for investors.

{kind=link}

However, caution is key. Despite the positive momentum, factors like ongoing remote work trends and high mortgage rates continue to impact certain real estate sectors. Investors should therefore approach these opportunities with due diligence, balancing enthusiasm with a strategic mindset as they explore top real estate stock options for 2024.

American Tower Corporation (AMT)

American Tower Corporation (NYSE:AMT), a leading global REIT, exemplifies industry excellence with over 28 years in the business. Headquartered in Boston, the firm manages an extensive portfolio of nearly 225,000 communication sites worldwide, including a significant presence in the U.S. and Canada. Recently, American Tower’s remarkable $14.86 billion in ETF-held stock earned it a spot among the Top 25 “Dividend Giants.”

Financially, AMT demonstrates robust growth and resilience. Despite a dip in net income, its third-quarter financials show a 5.5% bump in total revenue year-over-year (YOY), reaching $2.82 billion. This increase can be primarily attributed to a 7% growth in property revenue. Furthermore, adjusted EBITDA grew by 10.4% to $1.8 billion, underscoring the company’s solid financial footing.

Consequently, American Tower emerges as a compelling investment opportunity. Analysts’ strong buy ratings and a high estimate of $259, signaling a 20% upside potential, reinforce AMT’s position as a top choice for investors seeking growth and stability in the real estate stocks sector.

Realty Income (O)

Realty Income (NYSE:O), a standout in the real estate sector for 2024, saw a 9.69% dip in price in 2023, trading at a mere 1.32 times book value. This dip, however, presents a golden opportunity for income investors, particularly for those looking for long-term growth in retirement portfolios. Its resilience and proven track record in the market spotlight its potential as a robust investment.

Nevertheless, the company faces potential challenges, particularly from its upcoming acquisition of Spirit Realty Capital (NYSE:SRC), set to conclude in early 2024. While this expansion signifies strength, it also introduces risks of overvaluation and dilution, somewhat shadowing its immediate positive outlook.

Despite these headwinds, Realty Income’s foray into higher-risk sectors like gambling represents a bold strategic shift. This diversification, while risky, could offer new growth avenues. Considering its attractive 5.25% forward yield and current valuation, Realty Income stands as a compelling investment in 2024, blending risk with potential reward in the evolving real estate market.

Ventas (VTR)

Ventas (NYSE:VTR) stands out in the healthcare real estate sector. Celebrating over 26 years in the market and featured on the S&P 500, it commands an impressive enterprise value of over $31 billion. With 1,400 properties, Ventas effectively meets the rising demand for senior housing and medical facilities, boasting a significant 17% annualized return to shareholders since 1999.

In the third quarter, Ventas reported strong financial progress. Notably, net operating income increased by 5.1% YOY, and same-store cash net operating income soared by 7.9%. These solid results stemmed from higher occupancy rates and enhanced revenue per occupied room, alongside well-managed operating expenses, leading to a notable margin expansion.

Despite a net loss per share of 18 cents, largely due to non-cash impairments, the company’s dividend remains steady at 45 cents per share, yielding 3.53%. Analysts’ strong buy rating, with a target of $53 per share, underscores Ventas’s resilience and potential, positioning it as a solid investment choice in the evolving healthcare real estate landscape.

On the date of publication, Muslim Farooque did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.