Lucid Group (NASDAQ:LCID) is riding a wave of anticipation that it may have finally turned the corner. After a second-quarter deliveries update, Lucid stock hit a level not seen since last December.

Two weeks ahead of the luxury electric vehicle manufacturer’s second-quarter earnings report, investors are hoping Lucid found the right combination of production, price and incentives to generate sustained sales growth. They are now looking for clues this is the turnaround they have been waiting for. Wall Street is holding its breath too. Analysts have a collective hold rating on Lucid stock.

It won’t be production and delivery numbers that are being closely watched. We got those in the early July update. Rather it will be whether it can reduce its cash burn and not lose so much money on every vehicle produced.

Yet if Lucid pulls off an earnings beat on August 5, it could quickly reset price target expectations well above the $4 per share consensus view.

If that bullish scenario does play out in two weeks, don’t get into the driver’s seat. Use the new higher price point to take your money off the table.

Clearing Out the Logjam

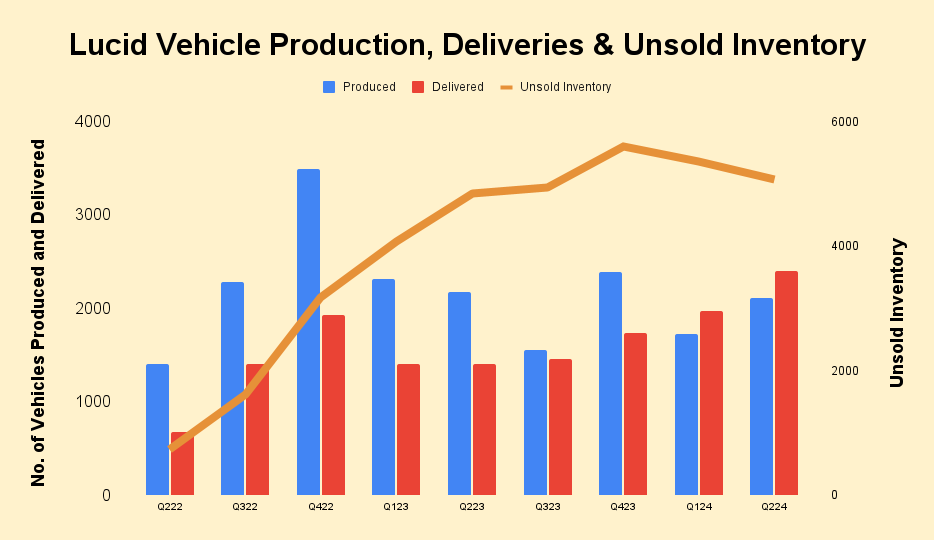

The production and delivery update earlier this month was a pleasant surprise. Lucid produced 2,110 EVs and delivered 2,394. It was the second consecutive quarter the automaker sold more vehicles than it made.

Yet Lucid is making far fewer vehicles than it previously did. Year-to-date, it has produced 3,838 EVs, or 14% fewer than last year. But it delivered 55% more cars than before. It indicates the EV maker is selling down a lot of older cars that have been sitting on dealer lots.

The problem is Lucid still has a significantly large inventory of unsold vehicles to work through.

{kind=link}

Data source: Lucid Group SEC filings. Chart by author.

In fact, it has almost 5% more cars gathering dust (5,075) than it did one year ago (4,848). They were down sequentially, which is a move in the right direction but dealers are going to need more incentives before they are willing to take on more inventory.

Cash Burn and Vehicle Losses

The company has cut prices on its base Air Pure at least three times. Part of that certainly comes from greater efficiencies, allowing Lucid to reduce costs that it is passing on. But it also indicates car buyers are still shying away from high-priced EVs.

The price cuts also don’t bode well for Lucid’s financials. It suggests the hoped-for reduction in cash burn and losses per vehicle won’t materialize or be as great as expected. Since Lucid is making fewer cars costs will naturally fall. But it may not be as organic as it appears on the surface.

Still, there is no bankruptcy on the horizon for Lucid stock. Lucid recently received another $1 billion cash infusion from the Saudi government’s sovereign wealth fund. At the end of the first quarter, Lucid had over $5 billion in total liquidity.

That is why you should not short Lucid stock. There is no danger of the EV maker going away.

Get Ready to Bail

Wall Street has a consensus hold rating on the stock. Price targets assigned in 2024 range between $2.90 and $4.50 per share. There are outliers as high as $12 a stub that was assigned in 2022 but never updated so it skews the outlook higher.

It is why investors should tread carefully with Lucid stock. We are going to see higher revenues just from deliveries rising both year-over-year and sequentially. But with likely fewer revenues per vehicle sold, it might not be the blowout the market is anticipating.

That could send Lucid stock reeling. Because there is so much uncertainty about the automaker, investors should get out of the stock and stay on the sidelines.

Lucid Group may find the magic elixir for generating sales and profits one day but that day is not now.

On the date of publication, Rich Duprey did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or

indirectly) any positions in the securities mentioned in this article.