EV giant Tesla (NASDAQ:TSLA) reported its hotly anticipated second-quarter (Q2) earnings on Tuesday. While the results largely beat expectations across key metrics, they were mostly seen as a wash, with Tesla stock closing in the red. Hence, follow the market on this one and sell Tesla stock.

The EV space is under major duress, but Tesla seems to be feeling the heat much more than its competition. With profits dwindling and sales substantially slowing, Tesla’s CEO Elon Musk focused on everything other than the company’s core EV business. During Tesla’s Q2 earnings call, Musk focused mostly on robotaxis, humanoid robots, and AI, overshadowing any discussion around a rebound in its core EV business.

Despite the challenging environment, Tesla stock had been up 77% in the past three months, reminiscent of its early days as a high-flying EV upstart. Tesla’s been mostly a forward-looking business, but its current valuation is unjustified. Consensus forecasts from Wall- Street analysts point to at least a 24% downside from current levels, with a substantial spread between its high and low estimates.

Mixed Q2 Showing

Tesla’s bulls are soaring following the automotive titan’s solid top-line beat of $760 million, pushing Q2 revenues to $25.5 billion. Another reason to celebrate was the 84.3% sales bump in its energy generation and storage business, which helped diversify its revenue base. On top of that, you have the robotaxi event scheduled for October 10, with Tesla’s humanoid robots set to potentially revamp internal operations by next year.

Yet, there’s a lot more than what meets the eye with Tesla’s Q2. The most glaring one is another earnings miss; it’s the fourth straight one. Its EPS of 52 cents missed estimates by a considerable 10 cents, its worst miss in recent memory.

{kind=link}

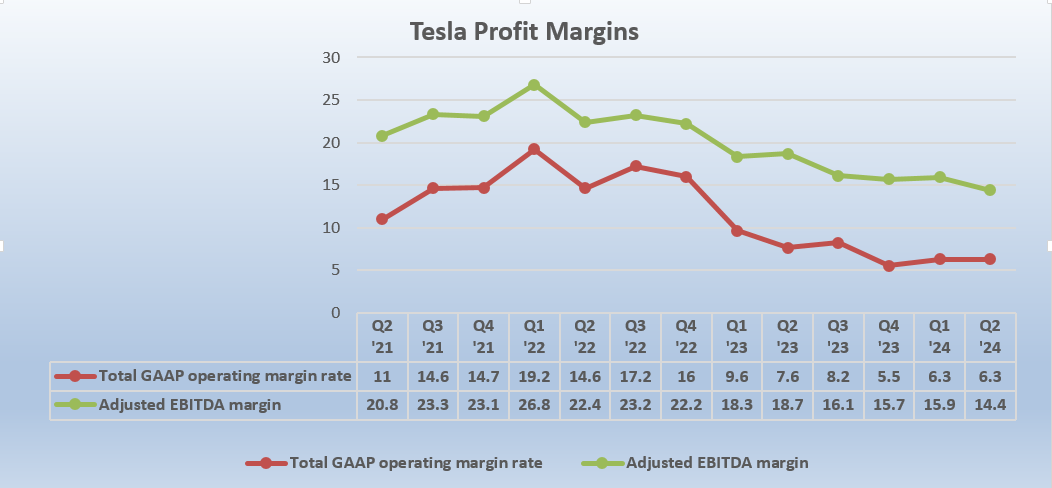

The declining trend in Tesla’s earnings is evident from the chart above. Operating margins have markedly slowed since the first-quarter (Q1) of 2023. A similar trend can be seen in its adjusted EBITDA margin from the third-quarter (Q3) of 2023.

The bulls would contend that though profits are waning in the current challenging economic conditions, Tesla is back delivering impressive revenue surges. To be fair, the $760 million revenue beat is impressive, especially considering the slowdown in the EV market. However, if we dive deeper, credit sales mostly drove these numbers. The EV pioneer generated almost $900 million by selling excess regulatory credits to companies that couldn’t meet emission standards. Strip $900 million from its $760 million beat, and you’re left with a $140 million miss.

Priorities in Question as Market Share Wanes

Reading through Tesla’s Q2 earnings transcript, I found myself instinctively double-checking to see if it’s still an EV company. That’s because over the past few years, the conversation has shifted from its core EV business to its other ventures.

As I mentioned earlier, Tesla’s AI, robotaxi, and supercomputer initiatives took center stage, masking weaknesses in its EV business. Regarding EVs, Musk made mostly tall claims that were largely unsubstantiated. He dismissed the price wars in the EV space, stating it will only be a near-term issue for Tesla. Moreover, without offering concrete details, he said the company was on track to deliver its first affordable model by early next year.

Nevertheless, recent reports suggest that Tesla’s neglect of its core business could have severe repercussions. Its dominance in the U.S. EV market is waning, with its share dropping below 50% for the first time in years during Q2. It held just 49.7% of U.S. EV sales during Q2, a decline from 59.3% from the prior-year period. If that wasn’t enough, Tesla’s struggles are mirrored in Europe, where sales dropped by 15% YOY, with its market share falling to 15.5% from 18%.

These numbers are troubling, even if Tesla is making headway in diversifying its operations. As it stands, it is still generating 78% of its sales from its EV division. Therefore, Tesla needs to up its game and strike a chord with customers drifting towards rival brands.

Bottom-Line on Tesla Stock

Tesla’s Q2 report suggests that its stock is remarkably overvalued. Its core automotive sector is floundering, with its margin profile veering off course. There are much better EV plays out there, which continue to impress with their numbers despite the market headwinds. I see little justification for holding a significantly overvalued stock like Tesla with skewed priorities. Therefore, it’s best to avoid TSLA stock for now.

On the date of publication, Muslim Farooque did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.