The stock market is now creating an opportunity for investors. Long-term tech stocks to buy abound, following some seriously negative sentiment and declining stock prices over the last month. The Federal Reserve heightened market fears when it raised interest rates by 75 basis points. Moreover, it cited the risk of inflation embedding itself into the economic system.

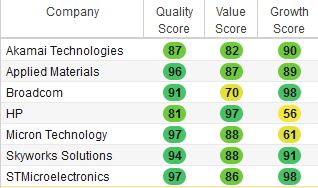

Technology stocks fell by 10% in September as a result. Their growth prospects fall as central banks tighten monetary policy, which could create a recession, or at the very least much weaker demand and inflation. Investors who run a stock filter for companies with strong quality, growth, and value may find the stocks in the table below:

{kind=link}

The seven selected tech stocks are high quality. This is important, as the economy deteriorates in the months ahead. Expectations are that these companies will be able to sustain strong returns on their invested capital. More importantly, their profit margins will not fall as much. Companies in the semiconductor and computer hardware sector are used to managing through business cycles. Accordingly, during severe downturns, these companies often cut expenses to protect profits.

Understandably, such companies may suffer from lower growth. In return, shareholders trade off this expected slowdown with better value. These companies’ value scores of 70/100 or higher suggest that investors have fewer downside risks in the long term.

| AKAM | Akamai Technologies | $86.02 |

| AMAT | Applied Materials | $89.21 |

| AVGO | Broadcom | $483.93 |

| HPQ | HP Inc. | $26.62 |

| MU | Micron Technology | $54.65 |

| STM | STMicroelectronics | $34.96 |

| SWKS | Skyworks Solutions | $93.19 |

Akamai Technologies (AKAM)

Akamai Technologies (NASDAQ:AKAM) Chief Financial Officer Edward McGowan appears bullish on his long-term prospects. The Akamai CEO recently said the company will report steady EBITDA margins. While unfavorable exchange rates hurt results, slower web traffic benefits Akamai. This company faces less impact from peak traffic, allowing the firm to save on capital expenditures.

To increase customer retention, Akamai passed its savings to customers in May 2022. For example, Akamai offered customers discounts. When business eventually rebounds, Akamai has the flexibility to increase hardware investments. Currently, capital expenditures account for only 2% of the company’s revenue.

Customers require Akamai’s solutions to manage their cyber security needs. Additionally, with the company growing its Enterprise Application Access offering, customers get enterprise-grade access to security. EAA is a small part of the overall business. This creates an opportunity for long-term growth, especially after the firm acquired Guardicore in October 2021.

Customers will keep investing in their digital supply chain despite the weaker economy. Additionally, these same customers will likely have new requirements for cybersecurity protection. Akamai offers them a safe user experience that will likely remain sticky over the long-term.

Applied Materials (AMAT)

Applied Materials (NASDAQ:AMAT) is a company with strong demand drivers that exceed supply concerns. That said, in this environment, AMAT stock is not reflecting this sentiment. Memory chip demand remains weak. Competition is heating up from Intel (NASDAQ:INTC), Samsung (OTCMKTS:SSNLF), and Taiwan Semiconductor (NYSE:TSM).

The market appears to fearing this weak memory demand, which overshadows Applied’s strength. Currently, this company is growing in the industrial automation and automobile markets. What may be an economic slowdown on the horizon is unlikely to hurt these strong sectors of the market.

In 2023, Applied is expected to enjoy relative strength in the foundry/logic markets. This will more than offset the weak memory chip market. In addition, the company will continue its investments in the 7-nanometer to the 3-nanometer manufacturing process. The company is progressing on increasing chip efficiencies as it overcomes various macro challenges.

The world’s conversion from gas to electric vehicles also benefits Applied Materials. The EV market requires more critical semiconductors in its supply chain.

Thus, as customers continue to invest in their digital infrastructure, I think Applied Materials is a great long-term tech stock to buy now.

Broadcom (AVGO)

Among the reasons I like Broadcom (NASDAQ:AVGO) right now is the company’s limited exposure to the consumer market. The economic recession many expect may thus skirt past Broadcom, as investors focus on more commercially-exposed names in the tech infrastructure space.

Broadcom is growing primarily from the strength in demand for the company’s infrastructure products. Broadcom benefits from a heavy backlog, which is unchanged at 50 weeks. On the supply side, Broadcom’s lack of exposure to China’s supply chain disruptions gives it an edge. CEO Hock Tan said that investors should expect the company to deliver growth of at least 5% annually for the long term. Even in a down cycle, growth that still averages 5% is notable.

Broadcom has strong long-term prospects, particularly in the company’s graphics processing business. Via SmartNIC video transcode, and its ASIC market, the company is expected to reach critical mass within the next three years. Although the company’s emerging markets business is not guaranteed growth, it is worth the long-term speculation. AVGO stock has a history of performing well in new markets.

HP Inc. (HPQ)

HP Inc. (NYSE:HPQ) spooked markets when it announced a decrease in demand for the company’s consumer products. Demand fell mainly due to the negative macroeconomic situation. Indeed, inflation and higher energy prices, plus the war in Europe, continue to provide a dampened outlook for PC demand moving forward.

That said, in HP’s commercial market, the company benefited from a strong quarter. This strong performance was met with tempered expectations, as investors sent HPQ stock sharply lower. Shareholders appear to be bracing for more conservative corporate orders.

Despite this stock’s price action, HP’s CEO, Enrique Lores, expects demand of 300 million units for the industry. More importantly, the addressable market for computers is bigger than before the pandemic.

Between 2020 and 2021, the pandemic shifted the dynamics of the PC market. Telemedicine, gaming, remote schooling, and hybrid work are trends that may be more permanent than many think. thus, customers will likely continue to demand HP computers to increase their productivity. As a result, strong long-term prospects for HP PCs could be the catalyst that increases profits.

HP’s average selling price is expected to rise by 20% to 30%. Even after factoring in supply chain constraints, better components and functionality will expand HP’s profit margins.

Micron Technology (MU)

Micron Technology (NASDAQ:MU) cut its utilization rates for the current quarter. The company now expects weaker NAND (storage) and DRAM (memory) demand will hurt margins. In addition, Micron must work through existing high inventories. By cutting production, Micron’s management team hopes this will position the company for the next technology transition.

Markets priced in Micron’s elevated inventory problems. With revenue and shipment volumes expected to decline, investors are taking the company’s commentary at face value.

That said, the company has also guided toward lower capital expenditures. Thus, there’s the potential that in the back half of the year, volumes will recover. Accordingly, cash flow could thus get a boost, and even turn positive, thanks to lower capital spending.

Micron is expected to benefit from selling at better DRAM prices, after supply growth recovers. In 2023, demand for memory chips is expected improve. Additionally, the PC market is shifting from the less expensive DDR4 memory to the faster DDR5 format. Accordingly, I think Micron’s average selling price could stabilize and potentially rise.

Investors are not paying much for MU stock. The price-to-earnings ratio is in the mid-single digits, around seven-times, at the time of writing.

STMicroelectronics (STM)

STMicroelectronics (NYSE:STM) managed relatively well through supply chain disruptions this past quarter. The company positioned its manufacturing to maximize output for high-definition-based products. CEO Jean-Marc Chery said that the company’s overall production of HD chips will increase by 12.5% in the third quarter.

Despite weak economic conditions in Europe, STMicro entered a seasonally strong period in the third quarter. Its operating expenses of $810 million to $815 million speak to this. Investments in the fourth quarter are expected to lead to higher returns after that.

Particular investments in the company’s Automotive and Discrete Group and Analog, MEMS, and Sensors Group are notable. That’s because these are strong markets with highly-engaged customers. Over time, expectations are that supply challenges in these segments will ease, benefiting investors in STM stock.

Additionally, in the company’s personal electronics sector, STMicro will benefit from strong traction. The company is gearing up for a recovery that accelerates later this year and into its fourth quarter.

Skyworks Solutions (SWKS)

Skyworks Solutions (NASDAQ:SWKS) has many strong opportunities in its core business. The company is extending its technology growth in the industry. For example, on the mobile side, Skyworks is diversifying its business. This should lead to higher growth and stronger earnings for investors.

In Skywork’s broad market portfolio, the company entered new end markets. CEO Liam Griffin said that the broad markets business is growing quickly. It accounts for 40% of the company’s overall business. This segment benefits from growth in data centers, handsets, infrastructure, and IoT markets.

In July 2021, Skyworks completed its acquisition of the Infrastructure & Automotive Business of Silicon Labs. This acquisition will allow the company to further benefit from scaling unique elements of its I&A unit. Already, Skyworks is seeing benefits from customer growth following this deal. Over time, it’s expected that Skyworks will be able to scale this business unit to a greater degree than the overall sector. Accordingly, I expect stronger profitability on the horizon, which could lift SWKS stock materially above its 52-week low.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.